Money can’t buy you happiness, but managing it effectively might help!

I’m sure we have all experienced the anxious feeling that arises when there just doesn’t seem to be enough money in the pot to cover all our expenses, or the gut-wrenching feeling that arrives when we are hit with unexpected and un-planned for expenses, like car and home repairs, or vet bills. Financial stressors are not uncommon and feeling overwhelmed by financial pressures is normal. It is when the stress takes over due to ineffective money management that our long-term mental health may start to suffer.

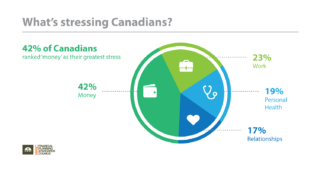

A nation-wide survey conducted on behalf of Financial Planning Standards Council (FPSC) showed that 42% of Canadians ranked money as their leading cause of stress, significantly more than work, personal health and relationships (FPSC, 2014). The survey also found that financial stress is contributing to poor sleep, reconsideration of past financial decisions, arguments with partners and dishonesty amongst family and friends about personal finances. When we lack sleep and our meaningful relationships are strained, a number of other problems can arise, and we can become overwhelmed, and our ability to cope with it all can start to wither away. When we are no longer able to effectively cope with these building stressors, and are stuck in a cycle of being stretched beyond our limits to try and make ends meet, we are at greater risk of experiencing long-term mental health difficulties.

It is often difficult for even the healthiest and wealthiest of individuals to effectively manage their money and the stress it may bring, but in individuals already suffering with mental health disorders or challenges, there is even more to consider. Those with existing mental health disorders are at greater risk of being affected by financial pressures for a number of reasons: (1) they may have less drive, focus, and motivation to properly manage their finances; (2) they may use spending money on desired items as a means to relieve symptoms; (3) they may be unemployed or on a leave from work for mental health reasons; and (4) they may be more prone to impulsive spending due to weakened inhibitions. In order to stay healthy, it is important for all individuals to develop a money management plan, and it is important for us to support one another in doing this because we will all fall victim to financial stressors of some kind. Researchers from The University of South Hampton concluded that the likelihood of having a mental health problem is three times higher among people who have debt, and that depression, anxiety disorders and psychotic disorders were among the most common mental illnesses people in debt experienced (Psychology Today, 2015).

It is a difficult and multifaceted challenge in that we can’t always identify the cause and effect – whether the debt caused the mental health issues or whether the mental health issues caused the debt – but regardless, both problems must be addressed. When you have an effective financial plan and are on top of things, it’s easier to improve your mental state – and when you are healthy, both mentally and physically, it is easier to take action on your debt.

So the answer isn’t simple, but it does exist. We must become mindful of both our mental health as well as our financial situation and if either are not where we would like them to be, we need to develop a plan. Seek counselling or reach out for social support if you notice that you are experiencing mental health difficulties, and seek financial advice if you are struggling to stay on top of things financially. You don’t have to try and do it alone – we are all in this together. According to a survey done by The American Psychological Association, 43% of those who say they have no emotional support report that their overall stress has increased in the past year, compared with 26% of those who say they have emotional support.

So here are some of our basic tips on tips on how stay mentally healthy.

(If you feel you need more support, in the form of coaching or counselling, we are here to help as well).

- Practice mindfulness & be mindful of your mental health

- Get adequate sleep

- Develop and strengthen your social support network (and use them!)

- Reach out for professional help when needed

- Engage in activities and relationships that are meaningful to you

- Set aside time for reflection to see whether you are truly living the life that you want to be living, and if not, make some changes

Because we are not financial experts, we reached out to a friend, Anton Tucker, who is a Certified Financial Planner and Portfolio Manager, and has many years of experience providing financial advice and support to people. We interviewed Anton and here is what he had to say about how to stay financially healthy:

‘’Managing money effectively is difficult because we are all so consumption driven. After all, our entire lives have been influenced by media touting the latest gizmo or paradise vacation that will “change our lives”. Most of us have also never been coached on how to properly ‘save the cents and in turn, grow the dollars’, so we are not to blame for not knowing how to do just that. Saving money is no different from exercising to get fit and stay in shape to be healthy. It requires a basic plan, discipline, patience and above all sacrifice. I believe in order to effectively manage our money we all need to first select a saving number based on our ability, need and life stage. The number is the percentage of your income that you will commit to save each and every paycheque. It should typically be 10%, 15% or 20% of your net income. In the simplest of terms, 10% will result in you being somewhat comfortable, 15% will deliver a good nest egg and 20% will provide a very solid financial base from which to fund an enjoyable lifestyle. Take this at face value as you contemplate your number and set about thinking how you can do this starting from your very next paycheque. You will be amazed at just how easy it becomes as you get used to setting this amount aside before you pay bills or think of spending again.’’

Staying on top of your mental health and your financial health simultaneously will go a long way in helping you stay mentally healthy and in not letting financial pressures threaten to take that away from you. Whether you are already struggling with mental health or financial stressors or are not yet, but still feel there is room for improvement, try some of the tips we have shared with you or reach out for more personalized support whenever needed.

APA. (2015, February). American Psychological Association Survey Shows Money Stress Weighing on Americans’ Health Nationwide. Retrieved from http://www.apa.org/news/press/releases/2015/02/money-stress.aspx

FCSP. (2014, November). Canadians Cite Money Worries as Greatest Source of Stress. Retrieved from http://www.fpsc.ca/news/publications-research/how-is-financial-stress-affecting-canadians

Georgopoulos, M. (2017, June). End the Stigma: Impact of finances on mental health (or the impact of mental health on finances…). Retrieved from https://www.linkedin.com/pulse/end-stigma-impact-finances-mental-health-maggie-georgopoulos

Morin, A. (2015, June). What Your Financial Health Says About Your Mental Health. Retrieved from https://www.psychologytoday.com/blog/what-mentally-strong-people-dont-do/201507/what-your-financial-health-says-about-your-mental

Richardson T, Elliott P, Roberts R. (2013, December). The relationship between personal unsecured debt and mental and physical health: a systematic review and meta-analysis. Retrieved from https://www.ncbi.nlm.nih.gov/pubmed/24121465